After a busy run of conferences and events, I finally had the chance to sit down with Citi’s 2025 Family Office Report.

It is always interesting to see what is happening at the big end of town globally, and this survey of 346 family offices with an average net worth of $2.1 billion offers a useful snapshot of how some of the world’s wealthiest families are currently thinking about portfolio construction, risk and opportunity.

A few themes stood out.

Despite a fairly uncertain global backdrop, family offices remain positive about portfolio returns.

According to the report, around 30% expect 12-month portfolio returns of 10–15%, with a further 8% expecting returns above 15%.

That is a fairly bullish stance given the current environment.

It suggests that while concerns remain elevated, many family offices are still prepared to lean into risk where they believe they are being adequately compensated.

One of the more interesting shifts in the report was what family offices now see as the biggest risks.

This year, trade tensions overtook interest rates as the top concern, followed by US-China relations and inflation.

That feels telling.

For the last few years, investors have been highly focused on central banks and the direction of rates. Now, geopolitical and policy uncertainty appear to be moving further up the list of things keeping large pools of capital awake at night.

In response to those concerns, 39% of family offices said they were leaning further into active management and shifting towards areas they viewed as more defensive.

That is not especially surprising.

Periods of uncertainty often create more appetite for selectivity, flexibility and manager skill, particularly when dispersion across sectors, regions and asset classes starts to widen.

Whether active management delivers on that promise consistently is another question, but the shift in sentiment is notable.

The biggest allocation winner in the report was private equity, with those increasing exposure materially outweighing those reducing it.

That continues a trend we have seen for some time.

Many family offices remain comfortable allocating significant capital to less liquid opportunities in pursuit of higher returns, control and access to private markets. But as always, the trade-off between return potential and liquidity deserves close attention.

That is particularly important in an environment where private market valuations, exit pathways and capital calls can become more challenging.

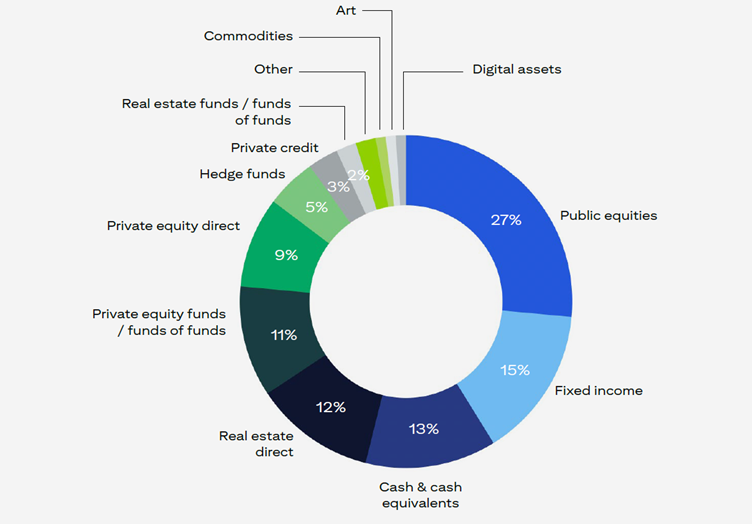

One of the clearest takeaways from the report is that alternatives remain a major part of family office portfolios.

According to Citi, alternatives account for around 40% of total asset allocation, with:

Meanwhile, the traditional core of portfolios remains:

All three of those core asset classes edged slightly lower compared to the previous year.

That tells its own story.

For many wealthy families, the portfolio is no longer built around a traditional mix of listed shares, bonds and cash alone. Increasingly, it is being shaped by private markets, specialist strategies and a broader search for diversification and return.

For those who want to dive deeper, the full report is here: Citi Family Office Survey. It is well worth a read.

If your wealth is becoming more complex and you would value greater structure, coordination and strategic oversight, without the cost of a family office you can learn more about my Virtual Family Office service here.

Kind regards,

Shelley Marsh

Outsourced Chief Investment Officer (OCIO) & Founder

Wealth Differently

General Advice Warning: Wealth Differently holds an Australian Financial Services licence to provide services to wholesale clients only. The information on this website is only for persons who are wholesale clients as per s761G of the Corporations Act. The information includes general advice which does not consider your particular circumstances and you should seek advice from Wealth Differently who can consider if the strategies and products are right for you. You should also understand that past performance is often not a reliable indicator of future performance and should not be solely relied upon to make investment decisions.

Wealth Differently Pty Ltd AFSL 547820.